By now, every risk and insurance professional in the country is aware of the tragedy that took place in Surfside, Florida on June 24th 2021. The collapse of the Champlain Towers South Condominium was one of the worst building collapses in our country’s history. The loss of life and utter devastation from this event is mind-blowing. As the reports came in about what may have occurred, the insurance nerd in me went straight to analyzing coverage.

Surveillance camera showing the 12-story condominium building in Surfside collapsing. NBC 6 South Florida.

One Degree of Separation to Insurance from Any Situation

We know that the property coverage for Champlain Towers South was through one of the Great American companies. What we don’t know are two things:

- The actual cause of loss; and

- If this was an ISO form or a proprietary form.

Focusing on Ordinance or Law Exposure

Preliminary information shows the structure was permitted for construction around 1979 and completed around 1982. Building codes were MUCH different back in those days. Miami-Dade County building codes were strengthened after Hurricane Andrew, which devastated that area in September 1992. Since then, Miami-Dade County has adopted the strongest building codes in the State of Florida.

In March of 2001, the Florida Legislature enacted the Florida Statewide Building Code (FSB), which was effective for any structure permitted on or after March 1, 2002. That code was further modified effective March 1, 2012. FSB is the MINIMUM standard across the state. Individual municipalities can require stricter standards, and Miami-Dade County has done that. Based on this loss, those that live or write property coverage in Florida can expect that both state and local codes will be strengthened going forward.

What does this mean for Ordinance or Law Coverage?

Under the ISO CP (Commercial Property) 04 05 – ORDINANCE OR LAW COVERAGE endorsement, coverage is split into three parts:

- Coverage A – Undamaged Portion of the Building

- Coverage B – Demolition

- Coverage C – Increase Cost of Construction

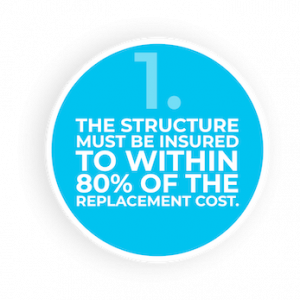

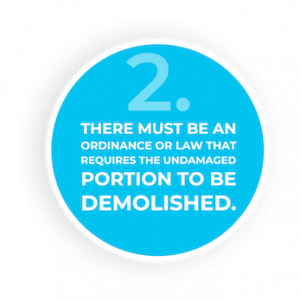

Coverage provided under the Coverage Form only applies to the damaged part of the structure. In the case of Champlain Towers South, a portion of the structure was still standing and was not damaged. Coverage A would pay for that portion of the structure that was not part of the collapse. Without Coverage A, the insurance company could have been within their rights to only pay for the portion of the structure that collapsed.

Three Requirements Needed to Activate Coverage:

Coverage B

Coverage B would pay for the cost to demolish and haul away the resulting debris from the undamaged portion of the structure. Debris removal for the collapsed portion would be covered, assuming it was caused by a covered cause of loss. An amount must be specified for this coverage, so it’s incumbent upon the agent to help the insured determine how much coverage is necessary. No one could have ever taken into consideration what happened regarding this massive collapse could, but the worst-case scenario is what needs to be planned for.

Coverage C

Coverage C pays for the entire structure to be rebuilt according to the building codes that were in force at the time the loss occurred. Can you imagine the number of code changes made since 1979? In addition to that, consider how much time it will take to permit the new structure for construction. Codes may change prior to issuing a new permit. This can cause significant coverage gaps depending on the form used to provide coverage.

How do agents determine what insureds need for Ordinance or Law coverage?

Do your research. Most municipalities’ building ordinances or zoning laws are available online. When trying to determine how to write coverage, two things need to be taken into consideration:

- What percentage of the structure must be damaged; and

- What valuation method is used.

The good news is that the percentage can vary anywhere from 41% to 51%. The bad news is that valuation can vary significantly, which impacts the amount of coverage necessary. Valuation can be expressed as property value; replacement value; and property tax assessment value. As you can see, values can be substantially different depending on the valuation method used when determining how much the potential exposure is overall.

For example, imagine an insured lives in Leon County, FL. In that area, like many others, there are two separate codes that may apply depending upon if the structure is located inside or outside the city limits of Tallahassee.

In the example mentioned regarding code variance, watch how that variance applies:

- The City of Tallahassee Building Ordinance says that the structure would have to be fully replaced if the damage exceeds 50% of the PROPERTY VALUE. This is unclear because the term is not defined in the ordinance.

- Leon County, FL Building Ordinance says that the structure would have to be fully replaced if the damage exceeds 50% of the ASSESSED VALUE. This is a very low threshold to hit.

Both ordinances state that if the Fire Marshall declares the structure unsafe, then it must be torn down and reconstructed.

What about potential building code changes that occur after loss and before permitting?

As mentioned above, this can cause a significant gap in coverage. No need to worry; the 2017 edition of CP 04 05 includes the availability of additional coverage for the Post-Loss Ordinance or Law. If the option box is checked and an additional premium charged, the endorsement will extend coverage to include any building codes that are effective after the date of loss, but before the day of permitting. This coverage applies provided the building codes must be complied with to get the permit for construction or a certificate of occupancy. No commercial property coverage that includes the building should be without this important coverage.

The National Alliance for Insurance Education & Research commends the first responders that came from all over the world to help with the building collapse in Surfside, FL. Thank you for your bravery and dedication.

Jay Williams, CIC, CRM, CRIS, MLIS, AIP, AAI, ACSR

Jay Williams started his insurance career in 1979. He spent 21 years in the agency business, 9 years at the Florida Association of Insurance Agents, and 7 years on the insurance company side of the industry. Jay was the interim CEO for Applied Client Network and CEO of a construction risk wholesale operation. Prior to coming to The National Alliance for Insurance Education & Research, he was an insurance educator, a consultant to agencies, companies, and industry partners, and an expert witness for both technical insurance and agent E&O cases. In addition to being an Educational Consultant, Jay is a member of the National Faculty, teaching CISR, CIC, Ruble Graduate Seminars, and PROFocus topics across the country.